In March of 2012 as quoted in Think Advisor Online, Susan John, Chair of the National Association of Personal Financial Advisors said:

“It would be a really rare circumstance where a reverse mortgage would fulfill a need for somebody. I’ve never done a reverse mortgage for a client for exactly that reason, ….there’s always a better alternative.”

However, In April of 2012, Dr Barry and Stephen Sacks wrote a paper that was published by the Journal of Financial Planning entitled: Reversing the Conventional Wisdom: Using Home Equity to Supplement Retirement Income

Since then, a total of 6 Articles, 82 pages, 34 Charts and Diagrams by 8 Different Author, 7 PhD’s, 1 JD, CFP’s and AIF have been published by the Journal. All focused on one single subject:

The Role of Reverse Mortgages in Retirement Planning

Here are the (6) Financial Planning Articles (as of November 2014)

- HECM Reverse Mortgages: Now or Last Resort? by Shaun Pfeiffer, Ph.D.; C. Angus Schaal, CFP®; and John Salter, Ph.D., CFP®, AIFA®

- Retirement Trends, Current Monetary Policy, and the Reverse Mortgage Market, by David W. Johnson, Ph.D.; and Zamira S. Simkins, Ph.D

- The 6 Percent Rule by Gerald C. Wagner, Ph.D.

- Increasing the Sustainable Withdrawal Rate Using the Standby Reverse Mortgage by Shaun Pfeiffer, Ph.D.; John Salter, Ph.D., CFP®, AIFA®; and Harold Evensky, CFP®, AIF®

- Reversing the Conventional Wisdom: Using Home Equity to Supplement Retirement Income by Barry H. Sacks, J.D., Ph.D., and Stephen R. Sacks, Ph.D

- Standby Reverse Mortgages: A Risk Management Tool for Retirement Distributions by John Salter, Ph.D., CFP®, AIFA®; Shaun Pfeiffer; and Harold Evensky, CFP®, AIF®

The Landscape has shifted, and once again financial thought leaders are taking a very serious look at the Role of Reverse Mortgages in solid fiscally responsible, proactive, eyes wide open financial planning. The March 2014 Journal of Financial Planning says it all.

“Historically, many seniors and financial planning professionals have viewed reverse mortgages negatively and considered their use only as a last resort. However, the three legs of the traditional retirement “stool” (Social Security benefits, pensions, and personal savings) have been considerably weakened by the factors described in this paper.

Current and future retirees need to re-examine their views and consider including a reverse mortgage as a part of their retirement plan. – Journal of Financial Planning (March 2014)

But let’s take a look at what started the entire discussion.

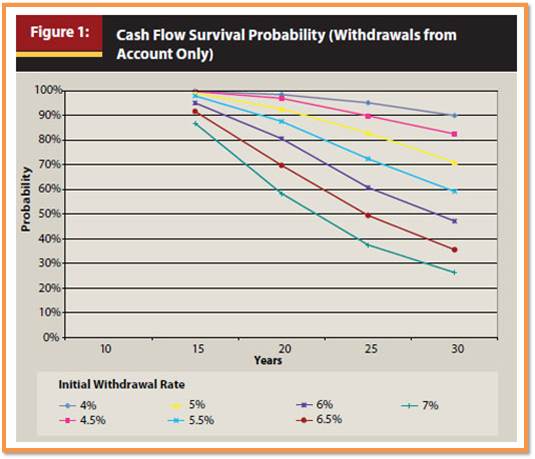

At What Initial Withdrawal Rate Do Clients Have The Greatest Chance of 30 Years of Savings

If a Planner Were to Add A Reverse Mortgage into a Planning Scenario Would it Make A Difference, and if so, When Would Inserting It Make the Most Impact

The 3 OPTIONS

- As a LAST RESORT: Use a Reverse Mortgage only when the savings have been completely depleted, or nearly so. Then and only then should you implement a Reverse Mortgage

- As a FIRST OPTION: Upon the onset of Retirement withdrawals, set up a HECM Line of Credit. Draw from the Reverse Mortgage as your sole source of income until it runs out and then draw from your portfolio. So a client in a $500,000 home sets up a $260,000 HECM. They have withdrawal needs of $4000 (but since they proceeds of the HECM are non-taxable and they are in a 25% tax bracket), they only need to take out $3,000 a month draw from the HECM. This will last them around 8-9 years. The HECM has a cost of living growth adjustment today of around 4%. So when they have finished drawing the HECM, then they draw from the plan

- As a COORDINATED STRATEGY: Set up the Reverse Mortgage at the onset of retirement. But in the year following a down market, draw from the HECM. If the following years return are negative, draw from the HECM again. In the year following at positive performance, draw for the savings.

Here’s what Dr. Sacks discovered:

Assuming a 5% initial Withdrawal Rate

Discovery #1

Using the RM as a last Resort gave the client a 76% chance of success vs. 70% without a RM at all. Statistically Insignificant! Using the Reverse Mortgage last has little to no impact on plan survivability

Discovery #2 and #3

Using the Reverse First Option or Coordinated Option gave the client a 94% success rate vs 70%. That statistical significance was overwhelming.

Simply stated. In their Research and through tens of thousands of simulations, they drew conclusive evidence that the best way to implement a Reverse Mortgage into a distribution plan was early and in a conservative and coordinated manner. Anything other than that for the majority of clients, was simply going to be the wrong this to do.

And thus began the movement by the planning community towards a fresh look at Reverse Mortgages.

Don Graves, RICP®, CLTC®, Certified Senior Advisor, CSA®

Latest posts by Don Graves, RICP®, CLTC®, Certified Senior Advisor, CSA® (see all)

- Unlocking Retirement Potential: Five Ways The Modern Reverse Mortgages Benefits Your Clients - May 28, 2024

- Redeeming Retirement Expectations | How a Simple Conversation Sparked New Hope in a Couple’s Retirement Dream - March 9, 2024

- Squeezing the Juice Out of Retirement: Understanding the Four Psychological Phases of Retirement - February 27, 2024

Categories: Accounting, Advisors, Banking, Financial, Financial Planning, Strategic Usage

Tags: Last Resort, Retirement Planning