One of the things on the minds of all advisors and clients is the question “Will I outlive my Savings”. Indeed a fair question given the advent of the Baby Boomers. They will live longer, have saved less and are more indebted than prior generations. The discussion on the table today is simple.

Can we Increase Portfolio Longevity with a Reverse Mortgage?

For part of this answer, we asked one of our industry partners; Security One Lending to help provide some answers. They in turn asked the financial planning software leaders Money Guide Pro to help us do a simple analysis to see if the Reverse Mortgage would make a difference.

HECM REVIEW: The Home Equity Conversion Mortgage (HECM) aka as a Reverse Mortgage allows a homeowner over the age of 62 to convert a portion of their homes value into tax free money. There are no monthly loan payments required, there are no standard income or fico score qualifications and they owners always remain on title to the home.

HOW CAN CLIENT HAVE THE PROCEEDS?: The proceeds can be taken as a lump sum, in a line of credit or as monthly payments. The payments can be in the form of a TERM (for a certain amount of time), or as TENURE (payments for as long as at least one borrower lives in the property)

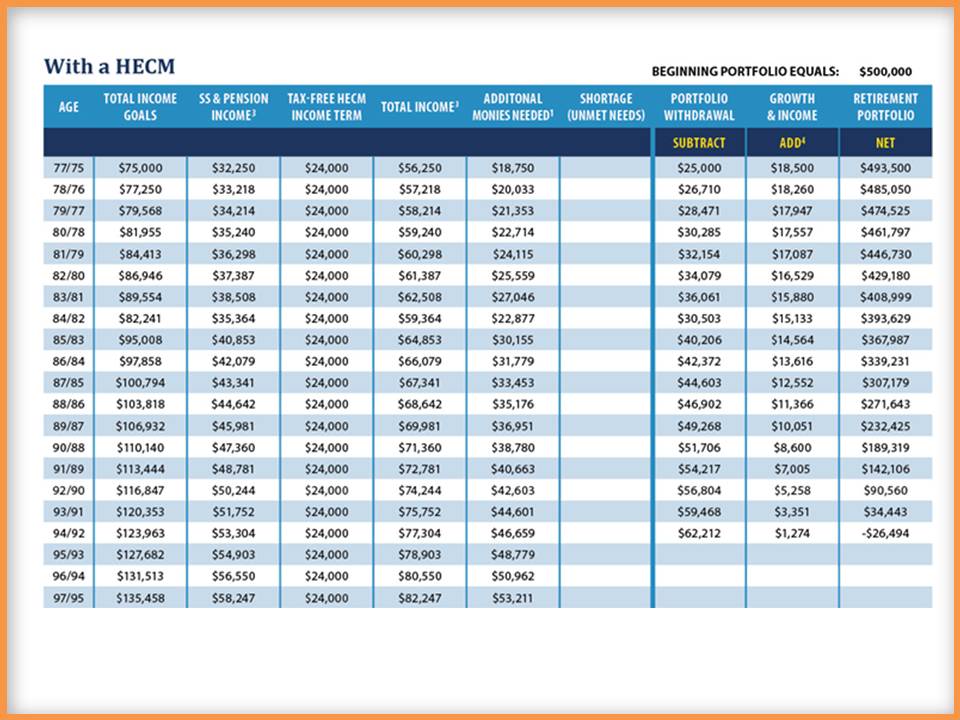

The following Illustration looks at a Tenure Payment stream.

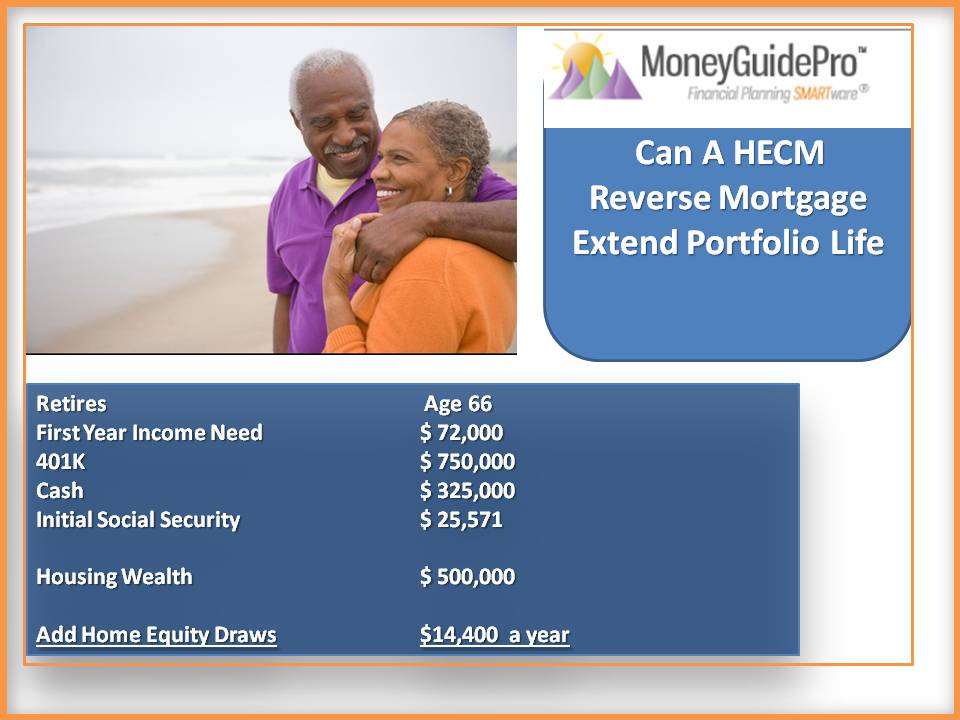

Here is our client. They have not done too bad in saving for retirement.

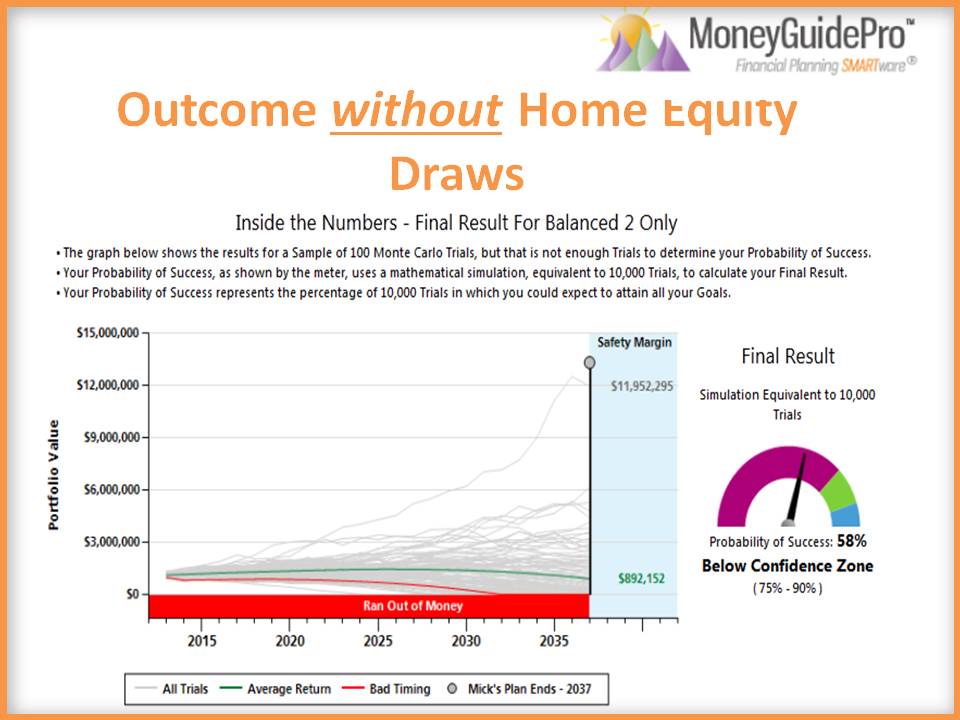

However, the financial planning analysis software after looking at all their numbers and running 10,000+ simulations predicts that their “Success” rate at 58%. That is, based on their input, they will either have to radically adjust their lifestyle or they will fall way short of their retirement goal of having enough money to last all of the retirement lives.

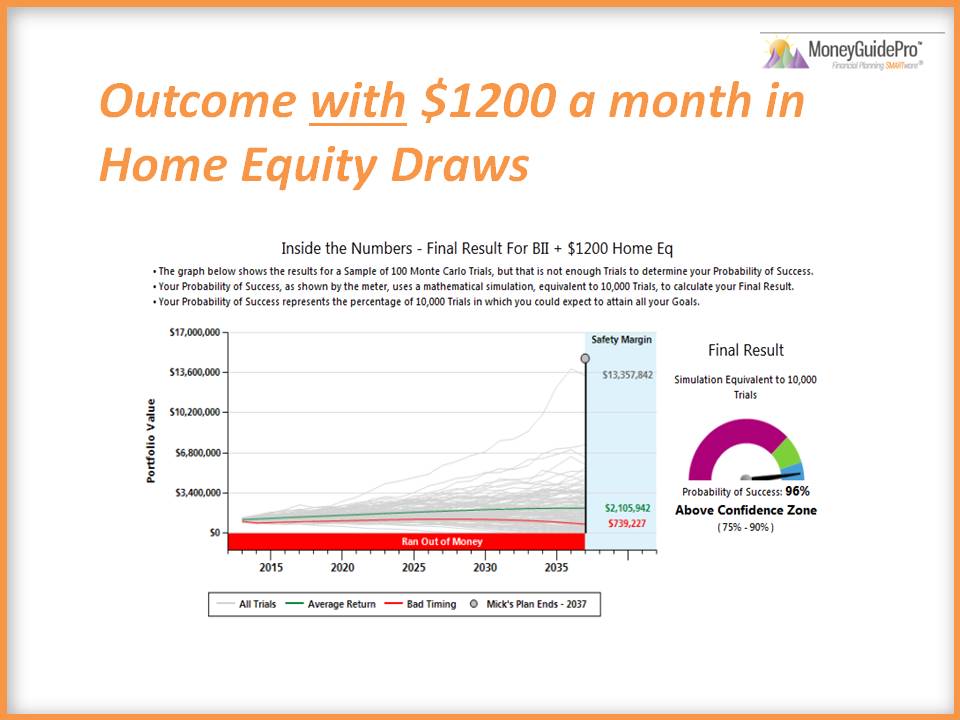

However, we now look at a borrower who chooses to implement a Reverse Mortgage and selects a monthly tenure payment of $1,200 a month (for as long as they live in the property). What is the Impact of such a strategy?

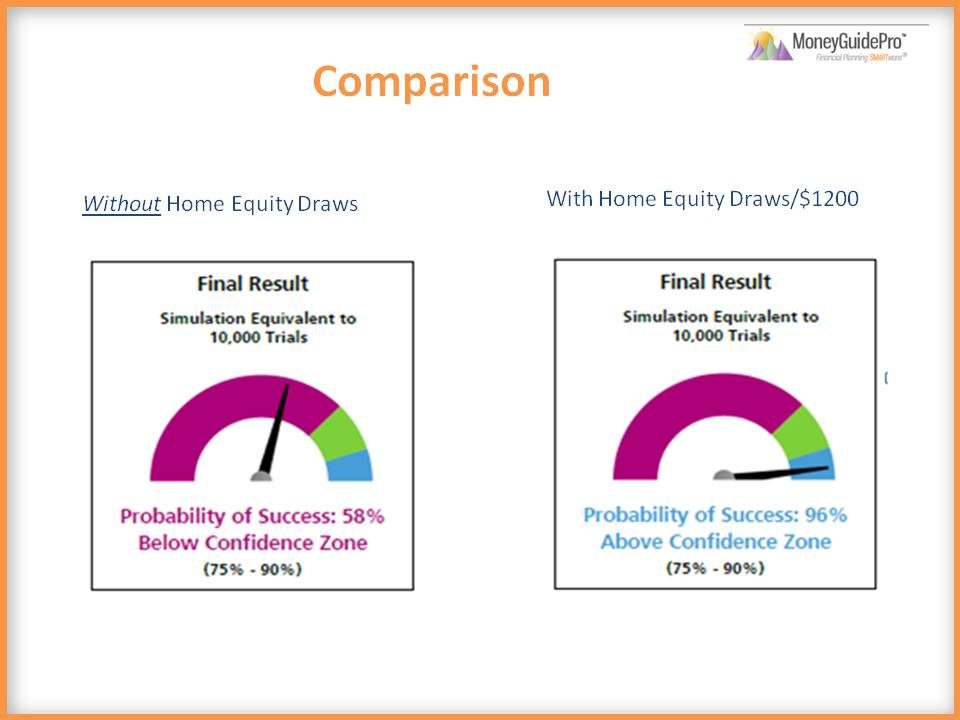

Clearly their advisor has placed them in a better long term retirement position by implementing this strategy.

- A confidence prediction of 96% vs 58% is stunning, for such a simple implementation. However, this was precisely the conclusions that the most advisors and financial thought leaders have come to since 2011.

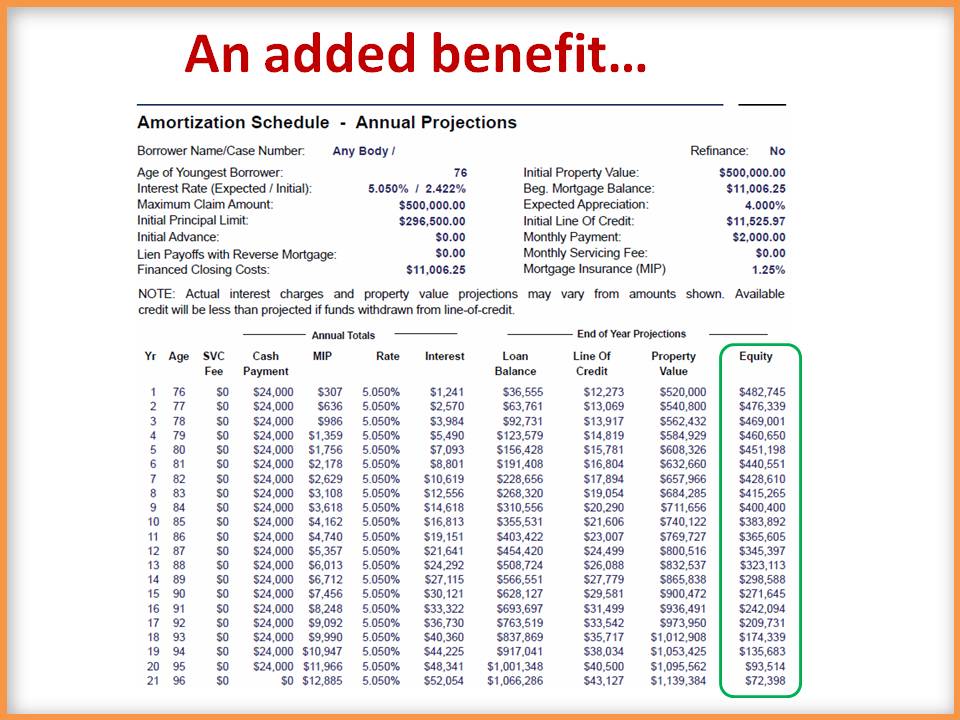

- An added benefit to this strategy is that there is Equity that remains in the property. See Below. Assuming the home appreciates at around 4% (which is a conservative estimate of appreciation over a 20 year period). It shows that there remains equity in the property.

NOTE: This example uses a total interest rate (Note + MIP) of close to 7%, where as total interest rates (3/2014) are closer to 4% for the standard line of credit. The point is that remaining equity is anticipated.

One More Example

I think you can follow this one

There we have (2) examples of what Financial Thought leaders and Advisors are modeling and demonstrating throughout the country. Which is:

A Conservative and Coordinated use of Housing Wealth (ie. Reverse Mortgages) can Greatly Change a Clients Retirement Outcome

Well Said.

Till next time.

Don Graves, RICP®, CLTC®, Certified Senior Advisor, CSA®

Latest posts by Don Graves, RICP®, CLTC®, Certified Senior Advisor, CSA® (see all)

- Unlocking Retirement Potential: Five Ways The Modern Reverse Mortgages Benefits Your Clients - May 28, 2024

- Redeeming Retirement Expectations | How a Simple Conversation Sparked New Hope in a Couple’s Retirement Dream - March 9, 2024

- Squeezing the Juice Out of Retirement: Understanding the Four Psychological Phases of Retirement - February 27, 2024

Categories: Accounting, Advisors, Financial, Financial Planning, Strategic Usage, Topics

Tags: Financial Planning, Running out of Money