How can the devastating impact that Sequence of Returns Risk poses to a retirees savings be mitigated by a Reverse Mortgage?

Every financial advisor understands the profound differences between the accumulation phase of a retirement plan and the distribution phase.

Primarily the dangers that come with beginning account withdrawals during a bear market. Better known as Sequence of Returns Risk or it’s close cousin; Reverse Dollar Cost Averaging. Today we want to look at how the HECM Reverse Mortgage can help mitigate some of those risks to accomplish genuine client satisfaction and savings that will last for all of their retirement.

In 2009 a large insurance company developed an initiative to show how clients could supplement their retirement income during economic downturns to avoid sequence of returns risk. (See press release Here and Booklet Here) Their work was fantastic and conclusions impressive. This article is not to endorse a company or provide a particular strategy, but rather to highlight the journey they outline and the impact of a diminishing portfolio due to withdrawal risks

I have drawn from some of that work (available online) in order to highlight its brilliance and also to add 1 or 2 more possibilities that simple were not known to most advisors at the time.

Lets look at a few slides

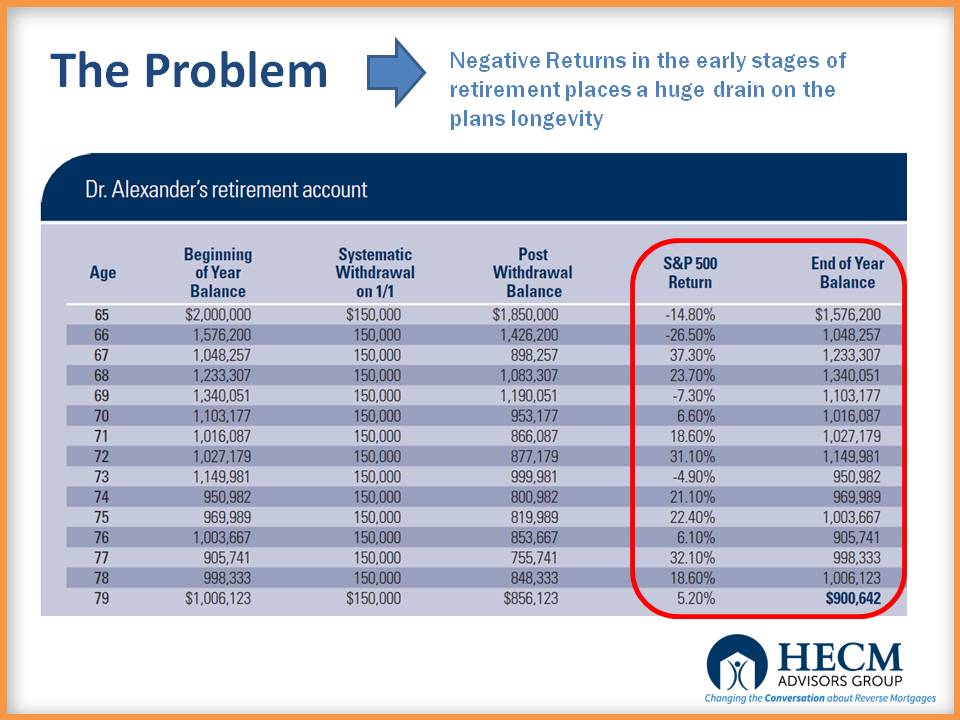

Meet the Good Doctor

Lets assume for a moment that we live in a perfect world. If the Doctor received a 6% return on her money with absolutely no fluctuation. If that were the case it would look something like this:

However, in the real world, that’s NOT the way markets function. They are up and down and sideways. And so lets look at a true life scenario:

Clearly the Doctor has done well in preparing for her retirement. The challenge is that the timing sequence beginning her withdrawals come during a bear market. Thus tremendously depleting her savings longevity.

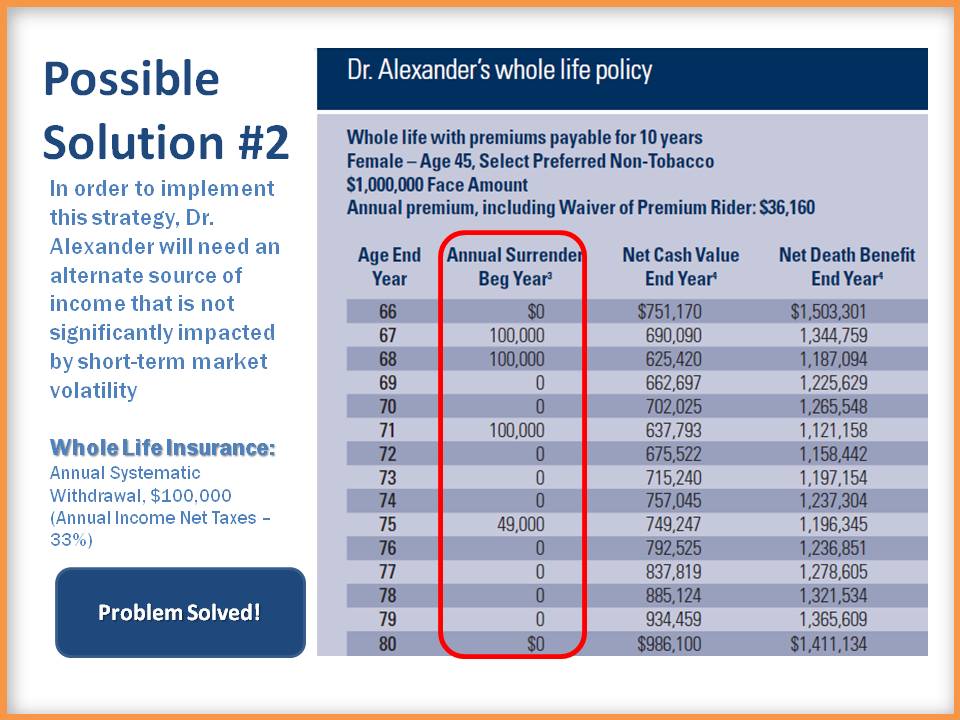

“Retirees who are able to supplement their retirement income during economic downturns by tapping the cash values of their whole life insurance policies could have a secret weapon to keep their plans on track during future recessions….By drawing on the cash values of their whole life insurance policies – and avoiding the sale of equities from their retirement accounts in a depressed market – retirees could end up with more cash and a larger net legacy to their families at death, while still meeting their retirement income needs”

That is the Challenge for this Scenario

3 Questions:

-

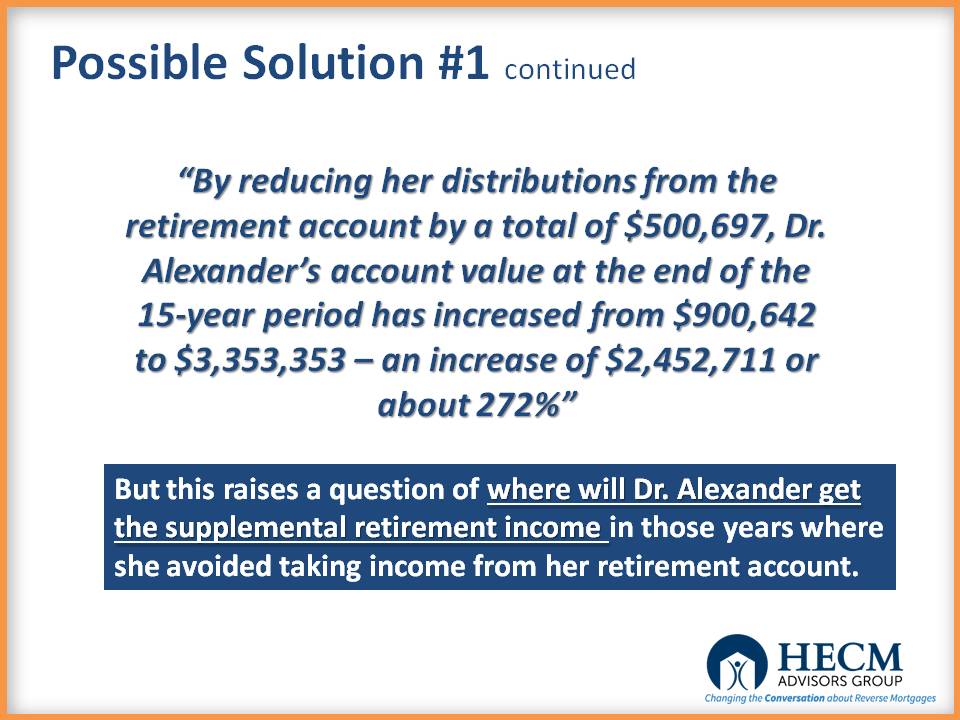

What if the Client did not have an Insurance Policy to draw from?

Then the client cannot implement this strategy

-

What if the client did not have ENOUGH Insurance in their plan

Then the client can only implement a partial strategy

-

Can the HECM Line of Credit be used as a Strategy?

It can be part of the Conversation

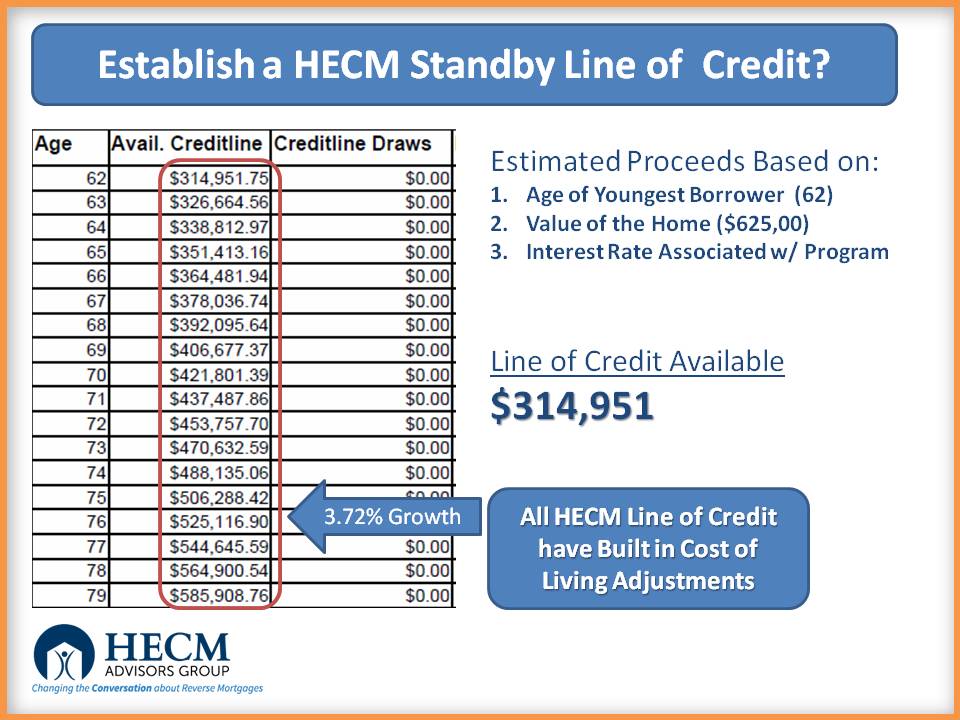

HECM Line of Credit

-

Dr. Alexander has a home valued at $625,500 and does not have a mortgage balance.

-

She discovers that she can set up a Reverse Mortgage Line of Credit of $314,951

-

This Line of Credit has a Cost of Living (growth) on the unused balance

So now the Client has obtained a HECM Standby Line of Credit with a Built in Cost of Living Adjustment. This Allows her to:

UPDATE – 12/2015 LINE of Credit available is $317,000

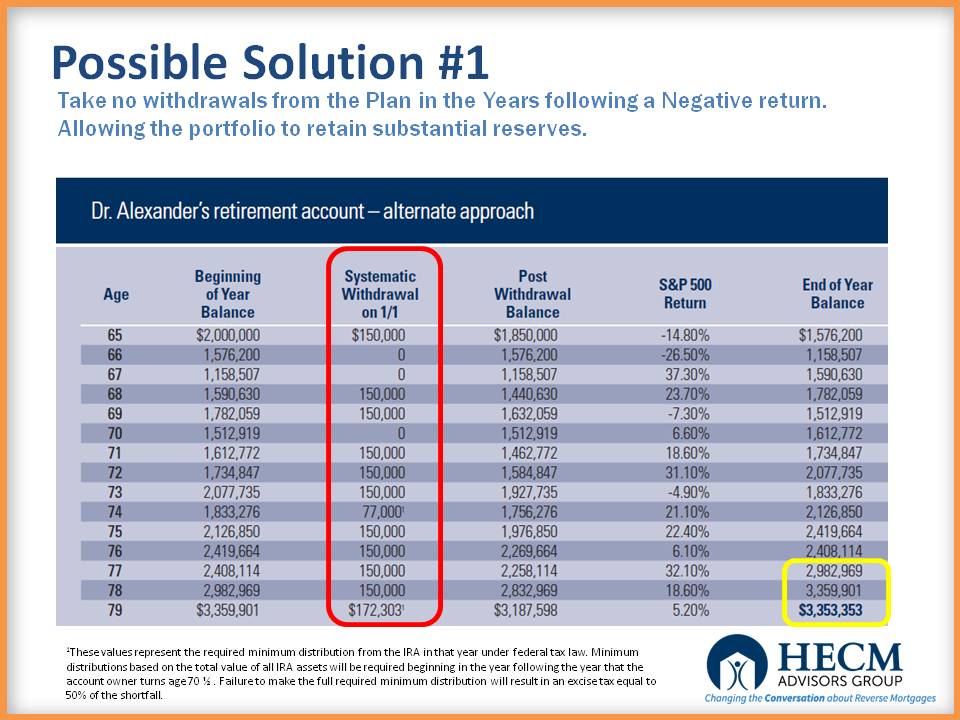

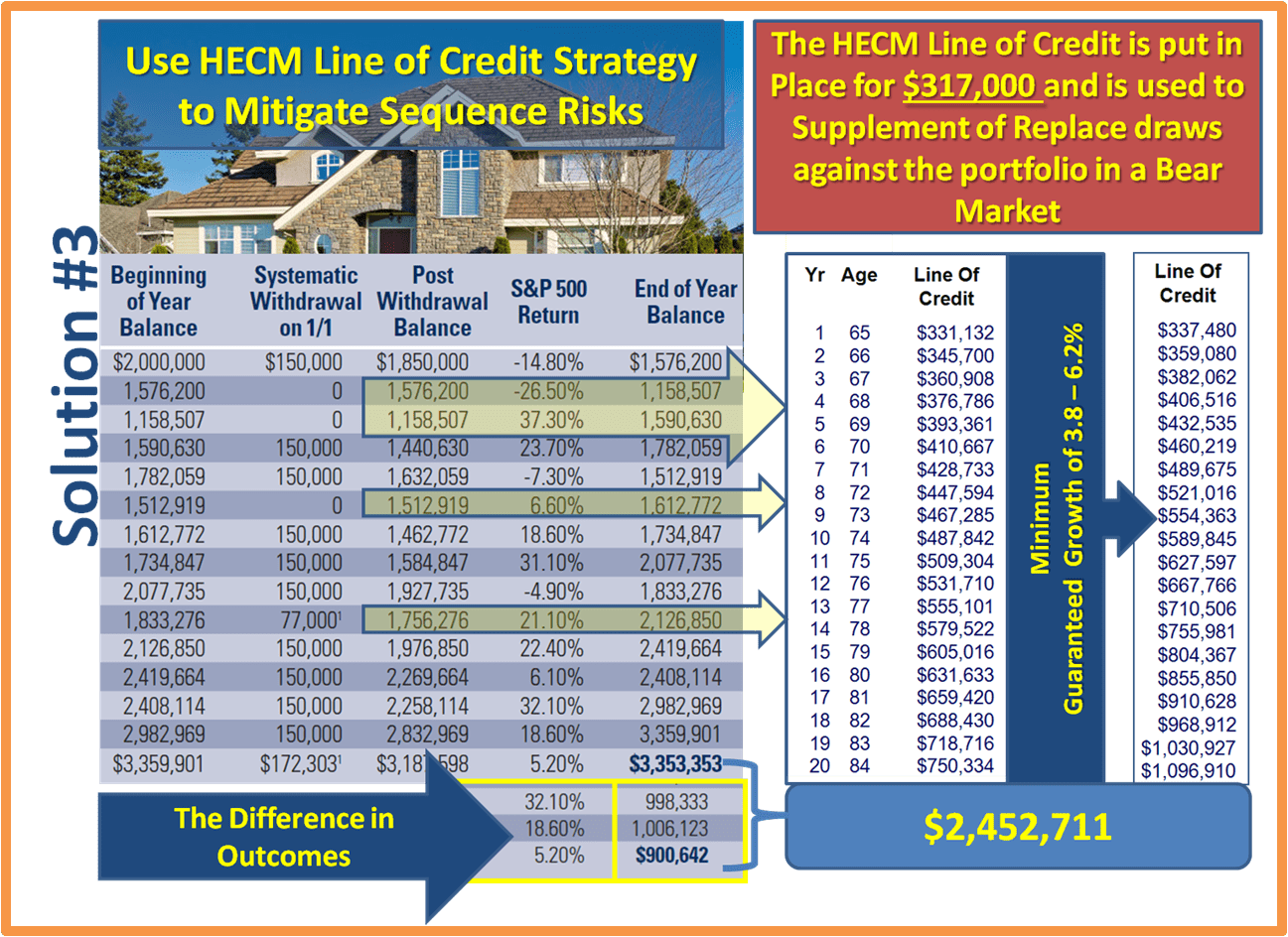

By Making this Simple Strategic Adjustment:

- She reduces the draw on the portfolio during a bear market and draws for the HECM.

- 15 years later, she still has a substantial amount in her savings and should sufficient to sustain the client at her lifestyle well into advanced years

- It was a legitimate Alternative

A Few Questions

1. What if the Client Didn’t Have Enough Life Insurance?

- The HECM strategy would allow the client to pull some funds from the Life Insurance and some from the HECM, creating even more savings survial probalitly and longevity.

2. What if the Client HAS Life Insurance but does not want to use it

- This happens when the client has a strategic LEGACY based purpose for the Life Insurance or it has already been borrowed against. The strategy still works. The client simply uses the HECM line to mitigate the portolio risks and leaves the Life Insurance in tact.

3. What if the Clients House was Not Free and Clear?

- Let’s stay the client had a traditional loan with a $200,000 mortgage balance and $1,600/month principal and interest payment

- Clients net income needs are $8,300 a month draw from portfolio

- If the HECM is used to eliminate an existing mortgage. Then draws from the portfolio need only net $6700 (a reduction of nearly 20%)

- Notice the Impact of reducing the draw on portfolio

- This does NOT take into account Sequence of Returns Risk, but it shows the powerful impact of paying off a mortgage (all things being equal)

- In ADDITION, the client still have a HECM Line of Credit of $115,000 to supplement portfolio withdrawals.

This is an excellent example of the negative impact that poor plan performance (early in the withdrawal stage) has on a clients retirement savings longevity. It also gives credence to the value of properly placed whole insurance into a clients financial plan, as well and a well crafted Reverse Mortgage strategy to supplement where insurance is not in place, not enough or simply not wanting to be used.

– Don Graves

Don Graves, RICP®, CLTC®, Certified Senior Advisor, CSA®

Latest posts by Don Graves, RICP®, CLTC®, Certified Senior Advisor, CSA® (see all)

- Unlocking Retirement Potential: Five Ways The Modern Reverse Mortgages Benefits Your Clients - May 28, 2024

- Redeeming Retirement Expectations | How a Simple Conversation Sparked New Hope in a Couple’s Retirement Dream - March 9, 2024

- Squeezing the Juice Out of Retirement: Understanding the Four Psychological Phases of Retirement - February 27, 2024

Categories: Accounting, Advisors, Financial, Financial Planning, Strategic Usage, Topics

Tags: Portfolio Preservation, Running out of Money, Sequence of Returns Risk