Retirement Risks

The market goes up; the market goes down. The television analyst says we’re in for a prolonged season of increasing gains, while a leading financial journal says we are now entering a time where market losses will be the norm versus the exception.

The idea of volatility, another market correction or a prolonged down market is scary for retirees. Unlike younger workers who can ride out the market and let their accounts recover, retirees are actively taking money from their investment accounts. It’s a very different picture – one that could be devastating to their retirement.

Sequence of Returns and Market Risk

Sequence risk involves the actual order in which investment returns occur. When a client regularly invests in a retirement plan, the movement of the market up or down will not have a huge impact because they have time to recover their losses. However, when the client withdraws money from their portfolio during retirement, they can end up selling more shares when the market is low—locking in losses rather than giving the market a chance to recover.

What can retirees do to offset the negative consequences of market volatility and sequence risk?

Can Housing Wealth Help?

They can use their Housing Wealth by drawing the money they need to live on from the reverse mortgage line of credit during the down years. Then they can replenish the line of credit when the portfolio recovers, or leave it as is. This is called the Coordinated Strategy.

It begins with establishing a reverse mortgage line of credit at the onset of retirement and then using some or all of it to cover income needs the year following a down year in the market. It functions as a type of asset class, but one that is not tied to the market, so it is safe from negative fluctuations and principal erosion. By doing this, retirees don’t draw from the portfolio – locking in the losses – but rather draw from the reverse mortgage giving the portfolio time to recover.

Furthermore, because the proceeds of a reverse mortgage are not taxable, they can draw less than what they would need to draw from the portfolio to receive the same amount and the line of credit can be used for other retirement income applications discussed in other articles.

Let’s take a look at one couple’s experience.

How One Couple Used Their Housing Wealth to Mitigate Sequence Risk

Couple A has $500,000 at the onset of retirement and takes a first-year withdrawal of $27,500. This amount is adjusted each year for inflation. Their advisor has a “reverse mortgage as a last resort” position. As the table shows, in the early years of their retirement, the clients experience some negative returns. This sequence now puts constraint on their portfolio, so that by year 24, they have run out of savings. They then establish a HECM and tack on another 7 years of retirement income—bringing them to a 30-year retirement. By most standards, this would be considered a success.

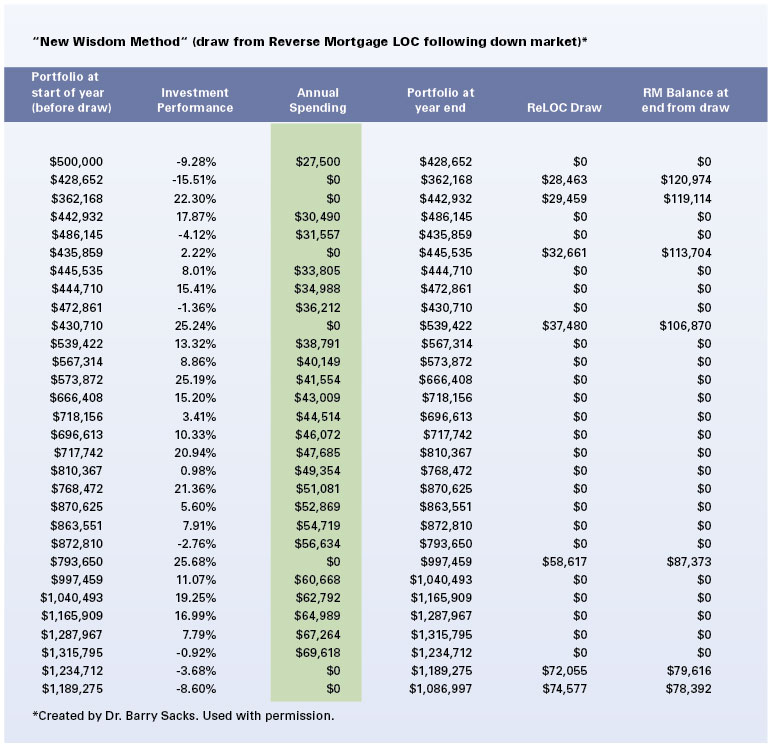

Couple B has the same starting point and withdrawal plan. The difference for them is their advisor suggests they do three things to mitigate both sequence risk and market risk:

- Establish a reverse mortgage line of credit (ReLOC) at the onset of retirement.

- Don’t withdraw any money from their retirement portfolio in the year following a negative return.

- Use a non-correlated asset to supplement the income they would normally draw from their portfolio.

The clients establish a $250,000 growing line of credit. In the years following a negative return, they draw from the ReLOC. By doing this, they eliminate the need to withdraw during a down cycle, thus preventing them from locking in losses.

Notice in the chart that by implementing this very simple strategy, the clients have substantially mitigated the sequence risk and, unlike the other couple, they have not run out of money in year 24. Instead, they have in excess of $1-million 30 years later. An extra million dollars!

With the implementation of a reverse mortgage, Couple B has a much more enjoyable retirement, the estate is greatly enhanced and their advisor keeps more assets under management for significantly longer (earning three times the fees earned by Couple A’s advisor). This is a win/win/win scenario.

Added Benefit

Because of the added financial security the ReLOC provides, Couple B no longer has to set aside two years’ worth of living expenses. Instead, they reinvest those assets–allowing for better returns than if they were left in a cash position. The ReLOC creates a much better buffer than having money in non-market performing positions.

The HECM line of credit is perhaps one the most powerful financial planning tools available today. The research, metrics, and illustrations all bear to these facts. The advisors who know how to implement housing wealth into retirement income plans will surely differentiate themselves, impact existing clients, attract new clients, and grow their practice.

Don Graves, RICP®, CLTC®, Certified Senior Advisor, CSA®

Latest posts by Don Graves, RICP®, CLTC®, Certified Senior Advisor, CSA® (see all)

- Redeeming Retirement Expectations | How a Simple Conversation Sparked New Hope in a Couple’s Retirement Dream - March 9, 2024

- Squeezing the Juice Out of Retirement: Understanding the Four Psychological Phases of Retirement - February 27, 2024

- Navigating the Three Economic Phases of Retirement: A Holistic Approach Using Reverse Mortgages - February 20, 2024

Categories: Advisors, Financial

Tags: Financial Planning, HECM Line of Credit, Portfolio Preservation, Reverse Mortgages and Retirement Planning, Sequence of Returns Risk, Wade Pfau